Dear subscribers, these are the analyses I posted to my paying subscribers, which, in hindsight, I should’ve made public to gain more traction on this newsletter.

Please keep in mind these returns are not annualized, it’s only been a bit more than half a year and if anything, too short a period to track real performance. Also, I wouldn’t buy lots of these current companies at their current prices because the margin of safety is somewhat diminished by the price increase.

I wanted to give you an update on my current portfolio. This update should not be taken as financial advice, I am just sharing my investing journey with you. We can learn from the mistakes I have made, and revel in the companies we got right.

I posted about a few companies earlier this year, so here is a brief update on what they are doing, and what I have done with them. I actually think most of these companies are still undervalued. I have learned I should hold a bit longer. I tend to sell too soon.

Also, when people tell you that ‘value’ has underperformed, please just remember that ‘value’ cannot be captured in an index labeled ‘value’. Value stocks are not ‘cheap’ stocks they are misunderstood companies trading at below intrinsic value.

Transglobe Energy. 90% Increase

March 9th (TGA $1.55 per share) TGA now trading at $2.95 per share.

Probably thought I was crazy buying this after a massive rally…but I don’t look at charts when I invest. Technical analysis is astrology for men. I buy on price.

I released an analysis on oil shortly after researching this company, oil is now above $80 a barrel. I am still holding onto significant amounts of TGA as I await their ratification with the Egyptian government to go through. The ratification, as described by their CEO, is going set to be ratified in Q4 this year.

The ratification will increase the amount of free cash flow TGA receives by a LOT. At current prices, it will cause a major windfall and investors will reap the benefits. I do believe there is a small risk the deal will not go through, but it is a risk I am willing to take.

I am slightly nervous that oil prices can sustain this level, but the democrats in major countries are seemingly making it hard for oil not to rise even above these levels, and a cold winter coupled with an energy crisis around the world (plus associated inflation) leaves me comfortable with my position.

Current position: I have taken profits at highs, but still hold a major position as I await ratification.

Uniti Group 20% increase

March 2nd (UNITI $11.40 per share) now at $13.65

I sold out of UNITI mid-year when I stumbled into Frontier Communications. I moved all my UNITI into FYBR (Frontier) because they are in the same industry but I believed FYBR to be way more undervalued. More on FYBR later. Even so, there was still value left in UNITI. Unfortunately, I didn’t share the upside.

Current position: Sold out at a loss as I moved into FYBR

Penns Wood Bankcorp, Inc 2% increase

May 7th (PWOD $24.17 per share) PWOD now trading at $24.65 with stable dividend

PWOD is a strange one. They didn’t experience the same run-up as the bigger banks, but insiders have been really stocking up on stock in insider trades. I am still holding because they are poised to benefit from higher interest rates. Their loan portfolio is interest-rate sensitive and stands to benefit from increased rates.

PWOD is sort of my inflation-hedged trade. I remain confident that insiders put their money where they expect to make money. Although to be honest with you, I do not understand this bank as well as I want to.

Current position: Holding

EzCorp 51% increase

April 5th (EZPW $5.16 per share) now $7.80 per share

I am still very fond of this company. When I found it lying low at the value I remember getting giddy once I started to understand the way their cash flows actually worked. Their financial statements were hard to decipher because their main business is in providing short-term loads. Management was also buying stock around $4-5 per share and I made sure to get my auditor buddy on a zoom call to make sure I was understanding the company properly (he is a master of accounting/accounting gimmicks). I had extremely high conviction about this company and wish I invested more into it.

Current position: Sold out at ~$8. The management is set on acquiring companies and I was hoping for buybacks…

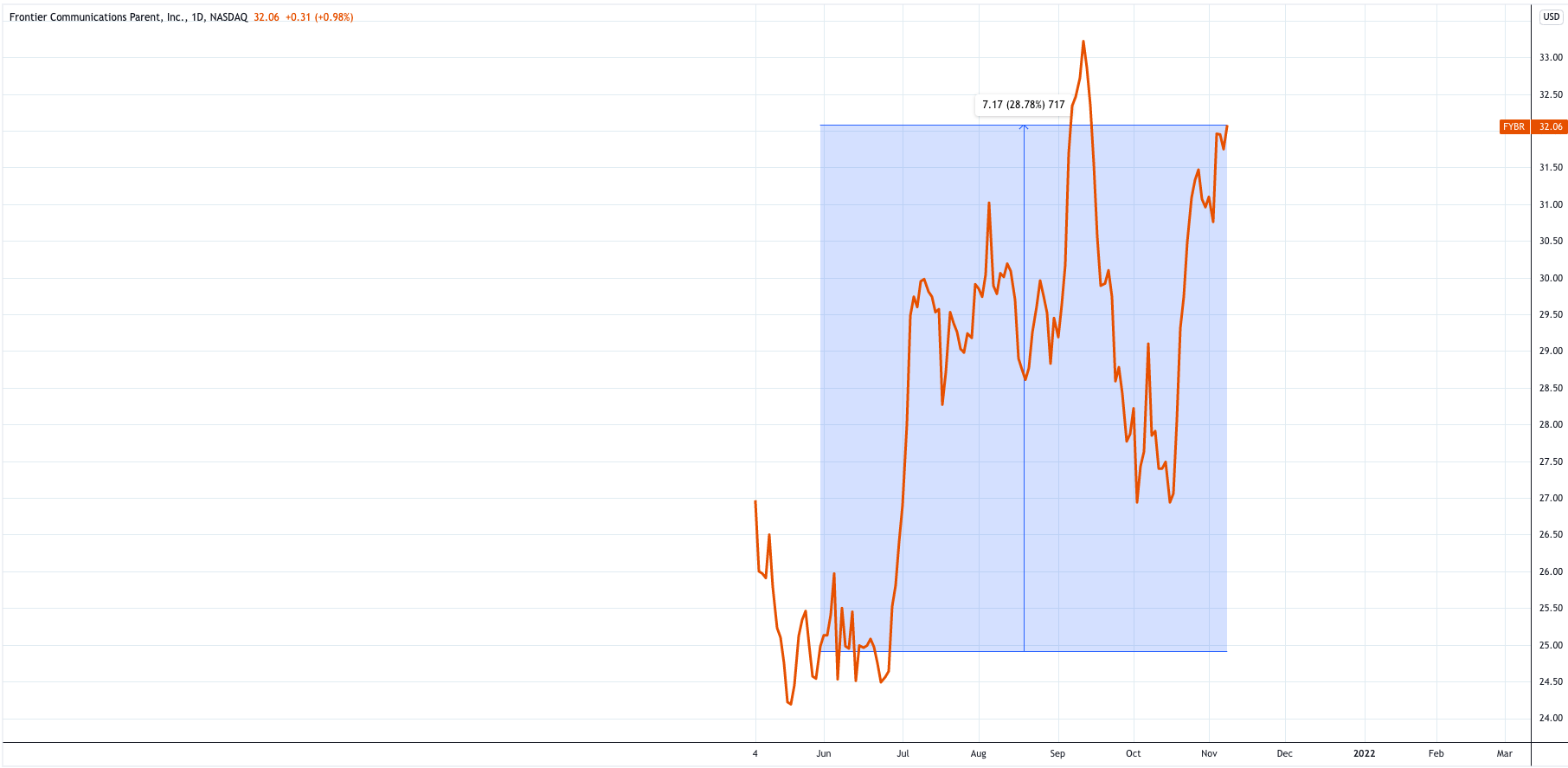

Frontier Communications 28% increase

May 28th (FYBR at $24.87 per share) now at $32.11

Frontier Communications was a darling find. They were rated the worst telecommunications company in the United States and even went bankrupt. I found them when they were emerging from Chapter 11 bankruptcy. $11bn dollars of debt were wiped off the balance sheet and they had a great reputable new management team. Most importantly, half of their assets were fiber lines, and fiber lines in the United States are hot property right now. They just signed an agreement with AT&T and I believe they are a prime take-over candidate.

Current position: I sold out out a portion of my FYBR when I read their new “fresh accounting financial statements” I believe the company, at current prices, maybe almost be fairly valued but I think their fiber assets still make them a good target for a take-over so I am holding a small amount of my original position.

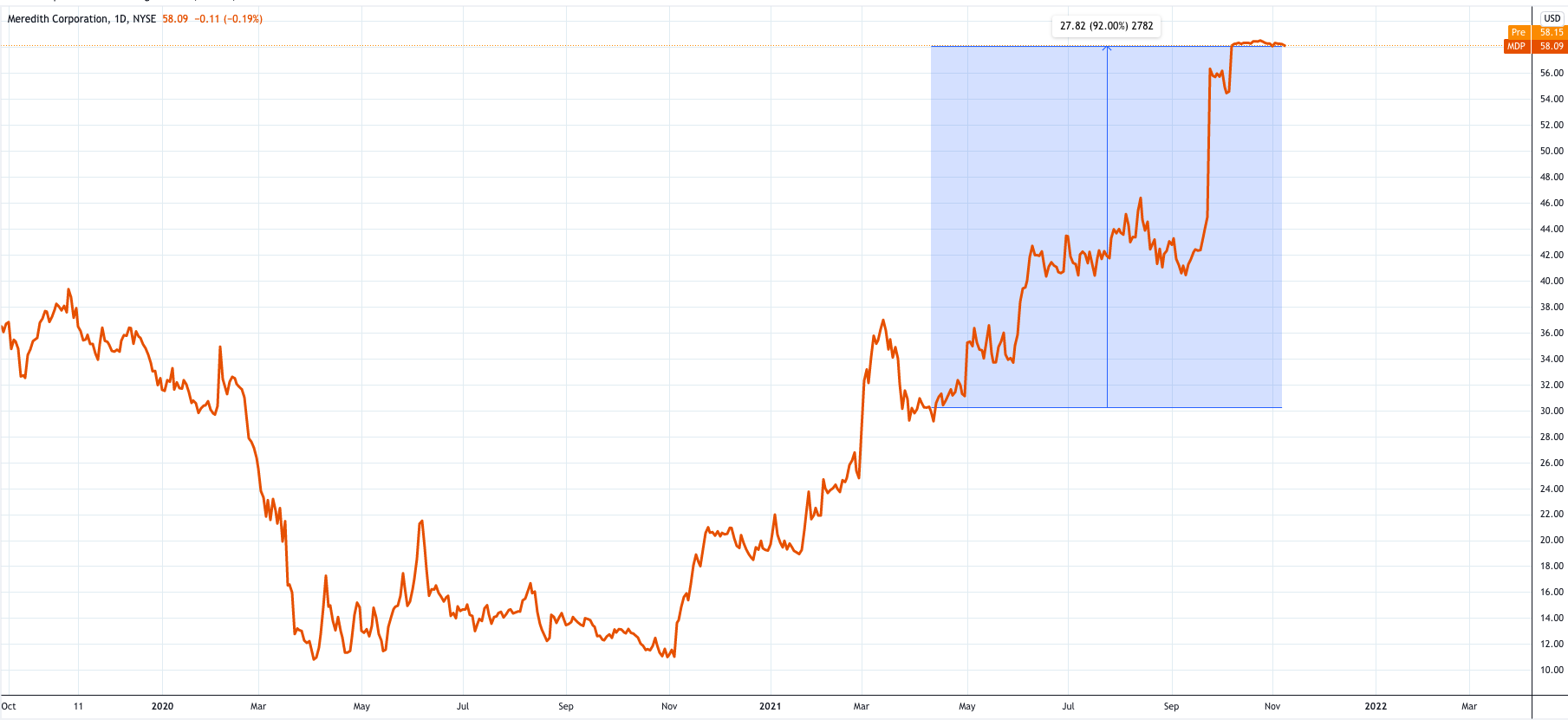

Arc Document Solutions 42% increase & Meredith 92% increase

ARC below:

I wondered whether it would be a good idea to add this here. Because I didn’t post about this company. I had the article saved as a ‘draft’ and then I fell ill. So I didn’t post. ARC document solutions was an easy company to understand. Management spent quite a few years trying to shift the company into a new direction and failed. Accumulated some debt in the process then paid it down…then the pandemic hit. I managed to find it in April.

Current position: Sold out at ~$3 something.

MDP below:

There is no link for Meredith because I didn’t post on it. The proof that I owned this is below. I just want to add it here so I have a sort of personal and public track-record.

This deserves a proper disclaimer. I sold Meredith very soon after I bought it, and only shared in maybe 20-30% of the upside. (And if you think I stole this from Burry, I bought this before his 13-F was released. Go confirm it for yourself).

My mistake was selling too early. They were and are a cash printing machine, the market misunderstood the fact that part of their business was growing very fast and the other half (the half the market was focusing on) was slowly failing.

Current position: Sold out completely, and too early!

AT&T and Discovery

I only recently posted my analysis on AT&T and Discovery so it’s too early for a graph (but Discovery is up a good ~10% since posting (market noise).

AT&T and Discovery are both undervalued in my opinion, but once I understood Discovery’s position in the soon-to-be merger I moved all my AT&T into Discovery. Discovery stands to benefit more from the merger and the real value is inside the Warner Media segment of AT&T. I believe the market will possibly dump the NewCo when it spins off, and then it will shoot up. But, at current prices, I believe Discovery is quite undervalued and in an industry (when coupled with Warner Media) to be valued at high multiples.

Current position: I hold a concentrated position in Discovery and no position in AT&T. I do think AT&T is somewhat undervalued but I already hold FYBR so I don’t need more exposure to the industry.

Why do I write these newsletters?

Lots of cool old rich dudes on Twitter keep asking this question: “Why sell your newsletter if you are making so much money on your stocks”. I mean the answer is simple. I’m young and therefore poor. I don’t have enough money to do this full-time (yet) and when I do, I will still publish because I am talking my book dummy!