EzCorp

I posted this for my paid subscribers a while back. EzCorp is up 10% since then, but I still believe it to be quite undervalued. It could easily do a reversal too, which would be nice because then I could load up some more.

BE CAREFUL AT THESE PRICES. I expect stock the retrace a bit first (don’t buy high and sell low lol)

Investing (real investing) is not just speculating on a ticker of a stock. It takes time. It takes reading financial statements and then reading and understanding financial statements. The distinction is huge. Some financial statements include line items and notes that ONLY the managers of those companies can even understand (if even). And we have often seen in the past that even auditors have lacked understanding when having direct access to those managers.

Fortunately, I think I can understand EZPW well enough to increase my odds of success substantially to warrant an investment. IF you don’t understand something about this analysis, leave a comment!

Introducing: EzCorp (EZPW) The ticker kind of sounds like “Easy Peasy” but I can guarantee you this was slightly harder to analyze, which is also why I think it hasn’t popped like the other value stocks.

Where do I begin?

not investment advice ladada haha. Sorry, this has to be here folks. This is not investment advice, this is purely educational content.

EzCorp: Pawnshop loans

EzCorp is a pawnshop that offers loans for collateral (which can really confuse you when you’re trying to calculate certain values like REAL free cash flow).

They operate 505 stores in the US. 368 stores in Mexico and 132 stores in Guatemala, El Salvador, Honduras, and Peru.

Stores in the US have been declining slowly (very slowly) year by year, but not in a dangerous fashion. Business in Mexico is strong and has been picking up over the last 4 years, leading to an overall increasing business outlook, increasing revenues, positive vibes until Corona.

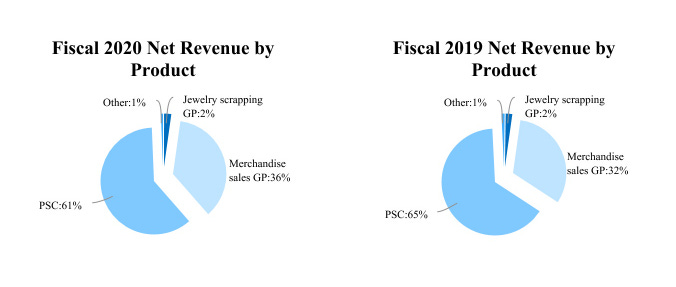

Most of EzCorp’s money comes from loan “service” charges, (basically just interest on the loans they give out). Redemption rate of close to 90% in the US. close to 80% in Latin America- people actually pay back these loans hooray.

I know how boring it can be to read text, so here’s a picture.

They trade at a net-book value (Total Assets less goodwill/intangibles less Total Liabilities) of $320 Million. This is ALSO excluding their investments in unconsolidated investments like their 34% ownership of Cash Converts in Australia (which is also significantly undervalued believe it or not) their 34% ownership of Cash converts is equal to $36 Million (US). Add that to the book value and you get a book value of $356 Million dollars of which $304 Million in CASH!

Huge margin of safety! Market Cap is only $280 Million! - EBIT is now $316 Million as of now.

Where does the confusion stem from?

So when I first looked at this company I calculated free cash flow, adding back your obvious non-cash charges like depreciation and amortization along with impairments. (Non-cash charges are expenses on the income statement that do not actually lead to an outflow of cash)

My free cash flow was around $10 Million per quarter, not enough to offer a good margin of safety or a good return into the future. BUT, I was wrong. Due to their business model, the more money they make, the more loans they give out, which is hard to understand looking at their financial statements because the loan outflows/inflows are all stated under their Cash Flow from Investments (Instead of Cash flow from operations). And the net-outflows are negative for CFI (cash flow from investments) because they are increasing their loans outstanding (a good thing).

When you look at their financial statements you will see under cash flows from investments they have been increasingly giving out more and more loans ( a good thing because they were building their loan portfolio before COVID hit.) This however confuses analysts (or maybe just me because I’m dumb as fuck) but this increase of outflows of money (that builds the loan portfolio) is like deferring profit to the future because they build up a bigger and better balance sheet but it doesn’t show properly on their income statement.

Until COVID hit, then you can see a huge unwind of this process, and BOOM they suddenly got a HUGE amount of cash inflow for two reasons 1: they made fewer loans 2: they kept selling forfeited loan collateral. So it essentially unwinded this operation.

So how do you try and understand what they are really making? So when we look at the NET outflows from their cash flow from investments, we miss something important. - NET increase in their inventory FROM the loan collateral. The net increase in their inventory (from forfeited collateral) does not show up on their statement of cash flows. BUT it does lead to future increased cash inflows. SO in order to calculate the CORRECT value added per year, we need to calculate the amount of cash inflow that WOULD be recorded from this NET increase in inventory per year.

Below is 2019 quarter by quarter. I calculate CFO subtract interest and tax and then the most important part. The yellow highlighted part shows the NET value change from the financing operations (the giving out of loans, + the repayment of loans + the money inflow from forfeited collateral + the net cash inflow that would result from their NET increase in inventory.) This last bolded part is the most important because it shows the net increase in cash they would receive from the net increase in their inventory from the forfeited collateral.

In the end, you can see a $50 Million real cash inflow.

2018 business looked EVEN better than this! And they had around $88 million of real cash flow (these numbers obviously fluctuate but the trend is upwards).

sorry if this is confusing. A lot of what you look at on a financial statement is due to accounting standards. Accounting standards can DRASTICALLY change what a company looks like on paper vs reality. And we need to try and use what we understand to get as close to reality as possible.

So what the fuck am I seeing?

Well before COVID, this business was doing fine and growing year by year through acquisitions into South America. The Stimmy checks however fucked everything up. But unless the government continues stimmying the fuck out of America, their business will pick up fast!

With the re-opening of the economy, this business already grew its loan portfolio back to $140 Million. When the stimmy check effect wanes off towards the end of the year I believe this company will be somewhat back to normal operations. With a big cash balance to start repurchasing shares or maybe a special dividend.

I do think the market could get spooked near-term because the effect the decreased loan portfolio will have on their income statement may be slightly profound, and the stock could drop to new lows. But the long-term of this business is still solid, and that is where 80% + of intrinsic value stems from when you look at a company using a net present value calculation.

So I will be picking up shares at the current price of around $5, and if the stock dips further I will pick up substantially more.

Long term trade:

More than 90% of a company’s intrinsic value is tied up to cash flows it receives AFTER 10 years! This means that the first 10 years only account for around 10% of intrinsic value.

If a company is in perpetual decline, then still around 76% of its intrinsic value stems from its ability to earn cash after 10 years.

Look at the picture below, this is a net present value calculation and it shows that only 26% of a company’s intrinsic value is from the next 10 years worth of cash flow.

So, what really matters is that the company will survive in the future. I believe EZCORP will do just that, as it was growing healthily before the pandemic, and with the re-opening, it has shown that its operations are getting back to normal.

CEO has been buying at these prices

CEO has been picking up small amounts of shares, he’s bought around $40,000 at current prices. Not a substantial amount, but normally people don’t just flush $40,000 down the loo.

Have fun chaps.