Aaron's Company Inc

Add this stock to your watchlist, it is already slightly undervalued, but not enough (in terms of my criteria) to offer a large enough margin of safety.

i.e I AM NOT BUYING YET

The short:

Aaron’s Company caught my attention after it spun off from Aaron’s Holding company in Dec 2020 into two separate companies. It displayed the signature post-spin-off swan dive that occurs from indiscriminate selling by funds with specific mandates (they have to sell), investors that couldn’t be bothered (they receive the stock in the spin-off and don’t want it), and possibly even day traders knowing that spin-off stocks tend to sell-off after a spin-off.

The two companies were; 1- Aaron’s Company (AAN) and 2- PROG holdings (PRG). Aaron’s Company is a lease-to-own furniture and appliances company. They service people without decent credit. They have 1092 physical locations around the United States.

Net earnings track closely to Free cash flows after capital expenditures.

Free cash flow: ~$120Mn after CAPEX per year (Free cash flow yield ~14%)

Market Capitalization: ~$813Mn

Debt: $0

Price to book: 1.18. (Excluding goodwill) P/B is a suitable metric to use since this isn’t a tech company - its assets are fairly liquid even in a fire sale.

Management has been using free cash flow to repurchase substantial amounts of stock. YTD (year-to-date) they have repurchased ~$90.4Mn worth of shares.

At a free cash flow yield of ~14%, 0 debt, and a history of strong cash flows which management first used to pay down debt, and then used to repurchase shares, Aaron’s has a decent margin of safety.

Biggest risk: inflation/rate increase. Due to the nature of this business, if we do see sticky inflation (which I think we will) the customers of this business will benefit at the expense of the company. The customers usually pay over a two-year period, inflation could eat into the margin, and constrain cash flow. Management knows this and decided to beef up the inventory going into the 4th quarter of this year. They are now running inventory levels higher than normal. I expect them to continue running a large inventory which may mean less cash flow for shareholders over the next couple of years.

The long:

Aaron’s has had quite a strategic overhaul by current management. On a net basis, they have been closing stores but revenue has been increasing. Management has seen progress with closing and consolidating different stores, as well as a new “central decision making” unit that allows them to cut costs by moving all leasing decisions to a centralized location that uses technology and data to make leasing decisions.

Store count (below) paints an ugly picture, but management has been clever with it. They are not willy-nilly expanding. They are consolidating some stores. Opening stores in new markets and renovating stores.

With so many stores closing, many investors may not see a future in this business. I am okay with this because I can discount the cash flows appropriately as you will see later, and assume this business eventually goes to 0, which is a high probability event given the competition it faces.

With an EV/EBITDA = ~3.2 this is one of the cheaper stocks on the market.

Short-medium term

In the latest earnings call, management admitted to the increased risk of inflation. It was due to this risk that they increased their inventory level, and are running a fatter inventory than normal. There is also only ~$60Mn remaining under their share-repurchase program.

At current prices, the company could repurchase 7.6% of the company thereby increasing the cash flow yield that remaining shareholders yield to higher than ~14%.

If we receive a filing from the company that the board has declared an increase to this ~$60mn amount it would mean that they still think the company is significantly undervalued and could provide decent support to the share price.

However, if we see inflation increasing the company may need to spare its cash flow to reinvest into inventory. Good for the long-term of the company, bad for the medium-term shareholder.

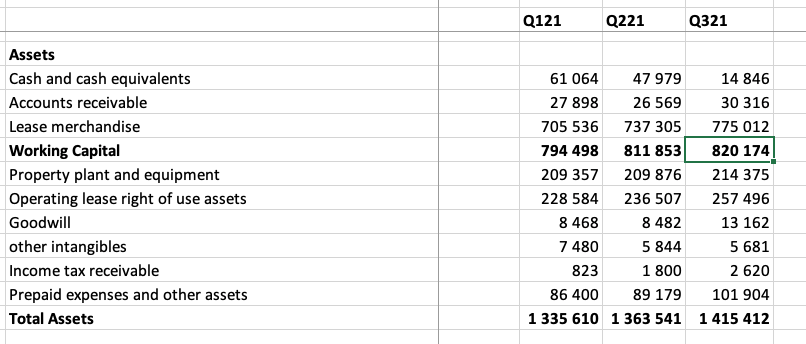

Take a look at the “Lease Merchandise” line item. That is cash flow that could have been available to shareholders. If we see inflation abate, these inventory levels can decrease, releasing more cash to shareholders - it may be enough to get us an adequate margin of safety.

Discounting the cash flows:

When I discount cash flows, I use a high discount rate (higher than necessary). I also assume the company will go bankrupt after about 20-30 years. (Not that it will, but then it gives us a really conservative estimate). If the sum of the present values is substantially higher than the market cap I know the company is relatively undervalued. Let’s take a look:

Mr. Market is saying that this company is worth around ~$800Mn (as of today) for that to be correct the following needs to happen;

Cash flows decline 5% a year for 10 years (which is not happening currently).

Cash flows then decline at 8% a year to perpetuity.

The company is essentially bankrupt after 20 years.

(I change the rate at which the company declines in my model to get it to that ~$800 market cap. This way I can understand what Mr. Market is predicting for the future of the company)

We can all see that maybe Mr. Market is extremely pessimistic towards Aaron’s. Under this assumption, only 20% of the company’s value is coming from after 10 years. (Look at terminal value 764 vs ‘after 10-year value’ of 149).

This calls for a simple scenario analysis:

Scenario 1 (worst case scenario): The market is correct and we still make a return of the discount rate of 10%. (not bad). Intrinsic value = current market value

Scenario 2: The market is incorrect and the company only goes completely bust after 30 years. Intrinsic value: $1Bn

Scenario 3: Company doesn’t grow but goes bust after 30 years. Intrinsic value = $1.2Bn

It is worth noting that the competitive pressures from Amazon and others could easily eat into this company’s business. But even in a worst-case scenario, the company seems to be ‘fairly’ valued. However, I still want a deeper margin of safety…

Margin of safety

I think this stock will appreciate in the medium term but I have become extremely averse to losing money and so I require a bigger margin of safety. A margin of safety arise can arise in a combination of these ways:

Competitive advantage: I don’t see one with Aaron’s. A company with a decent competitive advantage is a margin of safety in itself. If a company has an edge, it can weather an economic storm - and so can its shareholders.

Cheapness: Cheap stocks are generally cheap because they are boring, simple, and unloved businesses. Often they are too small for fund mandates. Some can even be value traps that end up in bankruptcy. However, once the research is done, and you understand the business well enough you can start looking to see if a margin of safety exists. With cheap stocks, I look for a margin of safety in:

The balance sheet: Low debt, highly liquid assets. Aaron’s company has this.

Cash flow yield: I generally want a cash flow yield of 20% (after CAPEX) if a business is leveraged. Aaron’s is not leveraged. Management is shareholder-friendly (and incentivized to be) so I know that most free cash flow should be directed to share repurchases. If a business is repurchasing shares while it has a cash flow yield of around 20% you can easily end up with a stock that is suddenly trading at a P/E of 5-4. Once that happens, the market generally reprices it to a P/E multiple of 10 and shareholders see a decent 100% gain on their investment. (At which point they should climb out).

In conclusion: I want a bigger margin of safety from Aaron’s before I climb in. And I understand that even at these prices it is quite attractive.

If you enjoyed this analysis, please share it.